Credit risk management strategies for lenders sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with casual but standard language style and brimming with originality from the outset.

In the realm of lending, managing credit risk is crucial for financial institutions to thrive and navigate the complex landscape of borrower uncertainties and economic fluctuations. This article delves into the core strategies employed by lenders to assess, mitigate, and manage credit risks effectively.

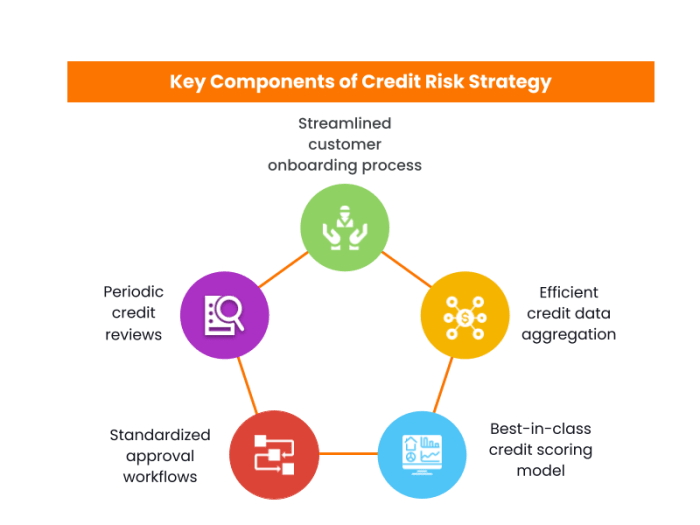

Overview of Credit Risk Management Strategies for Lenders

Credit risk management is a crucial aspect for lenders, as it involves assessing the likelihood of borrowers failing to repay their loans. Effective credit risk management strategies help lenders mitigate potential financial losses and maintain a healthy loan portfolio. Credit risk directly impacts the lending industry by influencing the interest rates offered to borrowers, the approval or rejection of loan applications, and the overall profitability of lending institutions.

High levels of credit risk can lead to increased default rates, which in turn can result in significant financial losses for lenders.

Examples of Successful Credit Risk Management Strategies, Credit risk management strategies for lenders

- Diversification of loan portfolio: Lenders can reduce credit risk by spreading out their loan exposure across different industries, regions, and types of borrowers. This helps minimize the impact of defaults in a particular sector or market.

- Use of credit scoring models: By utilizing advanced credit scoring models, lenders can more accurately assess the creditworthiness of borrowers and make informed lending decisions. These models consider various factors such as payment history, credit utilization, and income levels.

- Regular monitoring and review: Lenders should continuously monitor the credit quality of their loan portfolio and regularly review the credit risk metrics. This proactive approach allows lenders to identify potential red flags early and take appropriate actions to mitigate risks.

Types of Credit Risk Faced by Lenders

Credit risk is a significant concern for lenders as it directly impacts their ability to recover funds lent out. There are several types of credit risks that lenders encounter, each with its own implications for the lending process.

1. Default Risk

Default risk refers to the possibility that a borrower will not be able to repay the loan as agreed upon. This is one of the most common credit risks faced by lenders and can result in financial losses for the lender.

For example, if a borrower defaults on a mortgage loan, the lender may incur significant losses if the property value is lower than the outstanding loan amount.

2. Credit Spread Risk

Credit spread risk is the risk that the difference in interest rates between a risk-free asset and a risky asset will widen. Lenders are exposed to credit spread risk when they hold securities or loans with fixed interest rates. If the credit spread widens, the value of the assets held by the lender may decrease, leading to potential losses.

3. Concentration Risk

Concentration risk arises when a lender has a large exposure to a particular sector, industry, or borrower. If that sector or borrower faces financial difficulties, the lender’s portfolio is at risk of significant losses. For instance, a bank heavily invested in the real estate sector may suffer substantial losses during a housing market downturn.

4. Sovereign Risk

Sovereign risk is the risk that a government will default on its debt obligations. Lenders who hold government bonds or lend to foreign governments are exposed to sovereign risk. If a government defaults, lenders may face challenges in recovering the funds lent out, leading to financial losses.

5. Interest Rate Risk

Interest rate risk is the risk that changes in interest rates will impact the value of loans held by lenders. Lenders with a large portfolio of fixed-rate loans are particularly vulnerable to interest rate risk. For example, if interest rates rise, the value of existing fixed-rate loans decreases, potentially leading to losses for the lender.

Mitigation Techniques for Credit Risk Management

Credit risk management is crucial for lenders to minimize potential losses. Various techniques are employed to mitigate credit risk, ensuring the financial stability of the institution. Let’s explore some of the key strategies used by lenders in managing credit risk.

Proactive and Reactive Credit Risk Management Approaches

Proactive credit risk management involves identifying and addressing potential risks before they escalate. Lenders actively monitor borrower behavior, assess creditworthiness, and set risk parameters to prevent defaults. On the other hand, reactive credit risk management responds to issues as they arise, such as implementing collection procedures after a borrower defaults.

While proactive measures aim to prevent risks, reactive approaches focus on minimizing damage post-default.

Diversification as a Strategy for Managing Credit Risk

Diversification is a widely used strategy to manage credit risk effectively. By spreading loans across different industries, regions, and borrower profiles, lenders can reduce the impact of defaults on their overall portfolio. This approach minimizes the concentration risk associated with a single borrower or sector.

However, it is essential to balance diversification with thorough risk assessment to ensure that the portfolio remains resilient to economic fluctuations.

Technology Solutions for Credit Risk Management: Credit Risk Management Strategies For Lenders

Technology and data analytics play a crucial role in transforming credit risk management for lenders. By leveraging innovative solutions, lenders can enhance their risk assessment processes and make more informed lending decisions.

Examples of Technological Solutions

- Automated Credit Scoring Systems: These systems use algorithms to analyze borrower data and assign a credit score, streamlining the credit evaluation process.

- Big Data Analytics: Lenders can use big data to identify patterns and trends in borrower behavior, helping them assess credit risk more accurately.

- Blockchain Technology: Blockchain ensures secure and transparent transactions, reducing the risk of fraud and enhancing the overall credit risk management process.

Role of Machine Learning and AI

Machine learning and artificial intelligence (AI) are increasingly being used to enhance credit risk management strategies. These technologies can analyze vast amounts of data in real-time, identify potential risks, and improve decision-making processes.

Ending Remarks

As we conclude this exploration of credit risk management strategies for lenders, it becomes evident that a proactive and diversified approach is key in safeguarding financial stability and fostering sustainable growth in the lending sector. By embracing innovative technologies and leveraging data analytics, lenders can stay ahead of the curve and make informed decisions that mitigate potential risks while maximizing opportunities for lending success.

FAQ Guide

What are the main types of credit risks faced by lenders?

Common types of credit risks include default risk, concentration risk, and interest rate risk, each presenting unique challenges to lenders in managing their portfolios effectively.

How do lenders use diversification as a strategy for managing credit risk?

Lenders diversify their loan portfolios by spreading out their investments across different industries, regions, and types of loans to minimize the impact of potential defaults and reduce overall risk exposure.